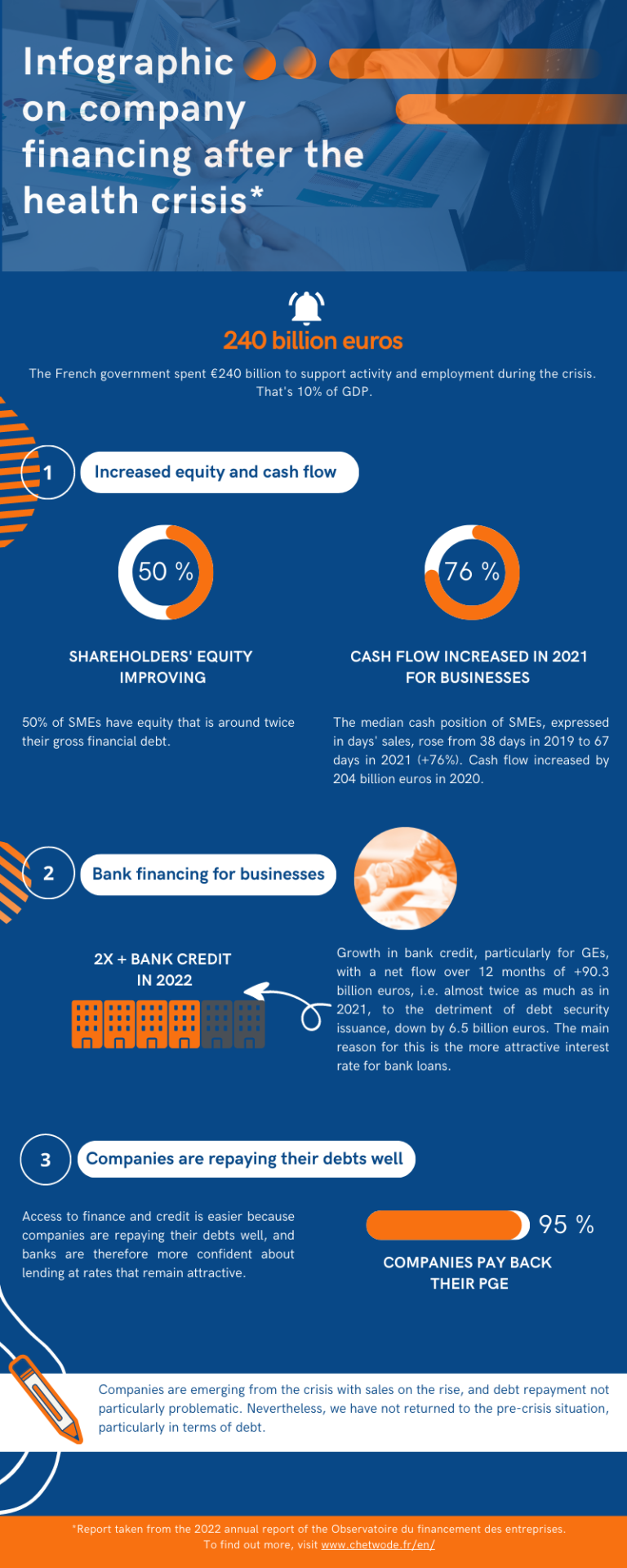

Did you know that the French government spent no less than €240 billion to support business and employment during the health crisis? This represents 10% of French GDP, according to the 2022 annual report of the business financing observatory, drawn up by the Banque de France in June 2023. This unprecedented support has been put in place to make it easier for companies to access finance.

As a result, companies as a whole were able to bounce back in 2021. Today, 3 years after the start of the health crisis that affected the whole world, we can see that, generally speaking, companies have recovered, and in some cases even exceeded, their pre-crisis sales levels (+5% for the retail sector, for example), although this is not the case for all sectors, particularly the accommodation and catering sector. We wanted to share with you our analysis of the economic situation, based on the Business Financing 2023 report. In this article, Julien Dufour explains the state of corporate debt today, after the crisis, before discussing the shift in the use of financing towards the financial system. Finally, he will look at the repayment of this financing.

To do this, we can look at companies’ leverage ratios.

First of all, we can see that these ratios are still higher than before the crisis. In the case of gearing (debt to equity), the rate was 86% in 2021 compared with 80% in 2019 for small and medium-sized enterprises (SMEs), or 134% compared with 119% for large enterprises (SMEs). The main reason for this is that, over the last two years, SMEs have succeeded in strengthening their equity capital, which has grown faster than debt, facilitating access to finance and reducing the debt ratio. In fact, 50% of SMEs have equity that is around twice their gross financial debt, reinforcing their financial strength. It should be noted, however, that here too we should not generalise, as almost a third of SMEs will experience a deterioration in their leverage by 2021.

Business financing can also be precautionary, in view of possible future needs and a rise in interest rates. At the start of the health crisis in 2020, financing was taken out in anticipation of weaker results. According to a report by the Banque de France, after a year in 2020 marked by an adjustment in spending, public aid and precautionary borrowing, we can see that cash flow improved in 2021 for businesses (of all sizes). The median cash position of SMEs, expressed in days’ sales, rose from 38 days in 2019 to 67 days in 2021 (+76%). This increase in cash flow coincides with a major rebound in gross operating surplus (EBITDA), up 38.5% on average. All these increases mean that companies have better access to credit.

In total, cash flow will have increased by €204 billion in 2020, while gross debt will have risen by €219 billion, driven in particular by the €141 billion increase in bank loans, driven by the distribution of EMPs. In 2022, net debt will increase after two years of very low increases: cumulative net debt flows will reach €80 billion.

We are now seeing growth in bank credit. In fact, there has been a shift from market credit (bonds, shares, etc.) to bank credit, particularly for GEs, with a net flow over 12 months of +90.3 billion euros, i.e. almost twice as much as in 2021, to the detriment of debt security issues, which are down by 6.5 billion euros. The main reason for this is the more attractive interest rate for bank loans. It is precisely against this backdrop that we can see that, for fear of a rise in interest rates, companies are now resorting to this anticipatory financing. This move towards credit is driven by the fact that fixed-rate loans are in the majority, thereby limiting the rise in these rates, which generally remain lower than those in other European countries.

There will be a decline in the number of requests for credit mediation, which will be particularly marked in 2022. This shows the resilience of businesses and their ability to repay their debts. This can also be seen in terms of companies’ ease of access to bank finance. As a result of this drop in the use of mediation by businesses, access to finance and credit is easier, because businesses are generally repaying their debts well, and banks are therefore more confident about lending, what’s more, at rates that remain advantageous.

Out-of-court restructuring of State Guaranteed Loans (SGLs) through Credit Mediation has been possible since 15 February 2022 under the conditions set out in a Market Access Agreement renewed in 2023, in addition to out-of-court procedures before the commercial courts. The aim is to find solutions on a case-by-case basis for companies facing difficulties. In the first year, only 671 applications were received. This can be explained by the fact that more than 95% of companies are repaying their EMPs in full, with more than €48 billion of the €143 billion granted repaid by the end of 2022.

So, perhaps counter-intuitively, we can see that companies are emerging from the crisis in a rather surprising way, with sales rising and debt repayment not posing any particular problems. Nevertheless, we have not yet returned to the pre-crisis situation, particularly in terms of debt. The crisis has also had an impact on interest rates, which are rising steadily. On 01/07/2023, the European Central Bank’s key rate will be 4%. This shift in lending from the market to the bank is explained in particular by the rate differential between the market and the banking system, which is more favorable to the latter. Will this trend continue in the long term, or will we see a switch back in the years to come? It’s difficult to say today. If you have any questions about financing your business, click here and we’ll be happy to help.